-

Join Us for a Farm Succession Presentation

Farm Succession: Planning Beyond Today Planning for the future of your farm involves more than passing down assets—it requires thoughtful consideration of financial, tax, and family dynamics to help ensure a successful transition. Ward & Uptigrove’s Agriculture Group invites you to attend Farm Succession: Planning Beyond Today, a complimentary presentation focused on helping farm families…

-

Staff Updates & Announcements

Staff Updates We are proud to congratulate the following staff members on their development and progression into new roles. Agriculture Department Progressions Zack Boertien Senior Accountant Tax Department Progressions Lydia Ossendyver Tax Manager New Staff Welcome! We are thrilled to welcome the following new staff members to our team: Joshua Dryden Tax Manager, CPA, CA,…

-

Landlord or Employer? Can it be both?

Landlord or Employer? Can it be Both? Short Answer: Yes, it can be both. Our HR Solutions team regularly hears from employer clients who include rental housing as a condition of employment. Employers need to know that they may become landlords under the Residential Tenancies Act, 2006, Ontario (“RTA 2006”) when they provide housing to employees. This…

-

Changes to Disability Tax Credit Application

The Canada Revenue Agency (CRA) has made updates to help process your disability tax credit (DTC) applications quicker. Updates to the DTC application are happening this summer. Key Dates to Remember Apply Using the Online DTC Application Form If you submit your application online through your CRA account, the CRA can process it faster than…

-

Veterinary Advisory Group Updates

Veterinary Advisory Group Updates Ward & Uptigrove Veterinary Advisory Webinars The Veterinary Advisory Group hosted a webinar in February where we discussed the following topics: If you missed this webinar and would like to view the recording, or any of our previous webinars, you can find them here: https://www.wardanduptigrove.com/webinar-recordings We welcome your input – if…

-

Competing for Labour – Veterinary Industry Ontario

How to differentiate your veterinary practice as an employer in 2026. We continue to see challenges attracting and retaining competent, qualified employees in the Ontario Veterinary sector. In 2023, we reported on trends in DVM recruitment; be sure to refer to that article to read about creative recruitment and retention ideas for your practice. For this…

-

Change from Paper to Online Mail for Some Individuals

If you are registered for a Canada Revenue Agency (CRA) account and currently receive paper mail, the way you receive your mail from the CRA might be changing. Since July 3, 2025, the CRA has implemented a multiphase initiative to transition approximately 1.3 million individuals from paper to online mail. As of May 28, 2026, the initiative…

-

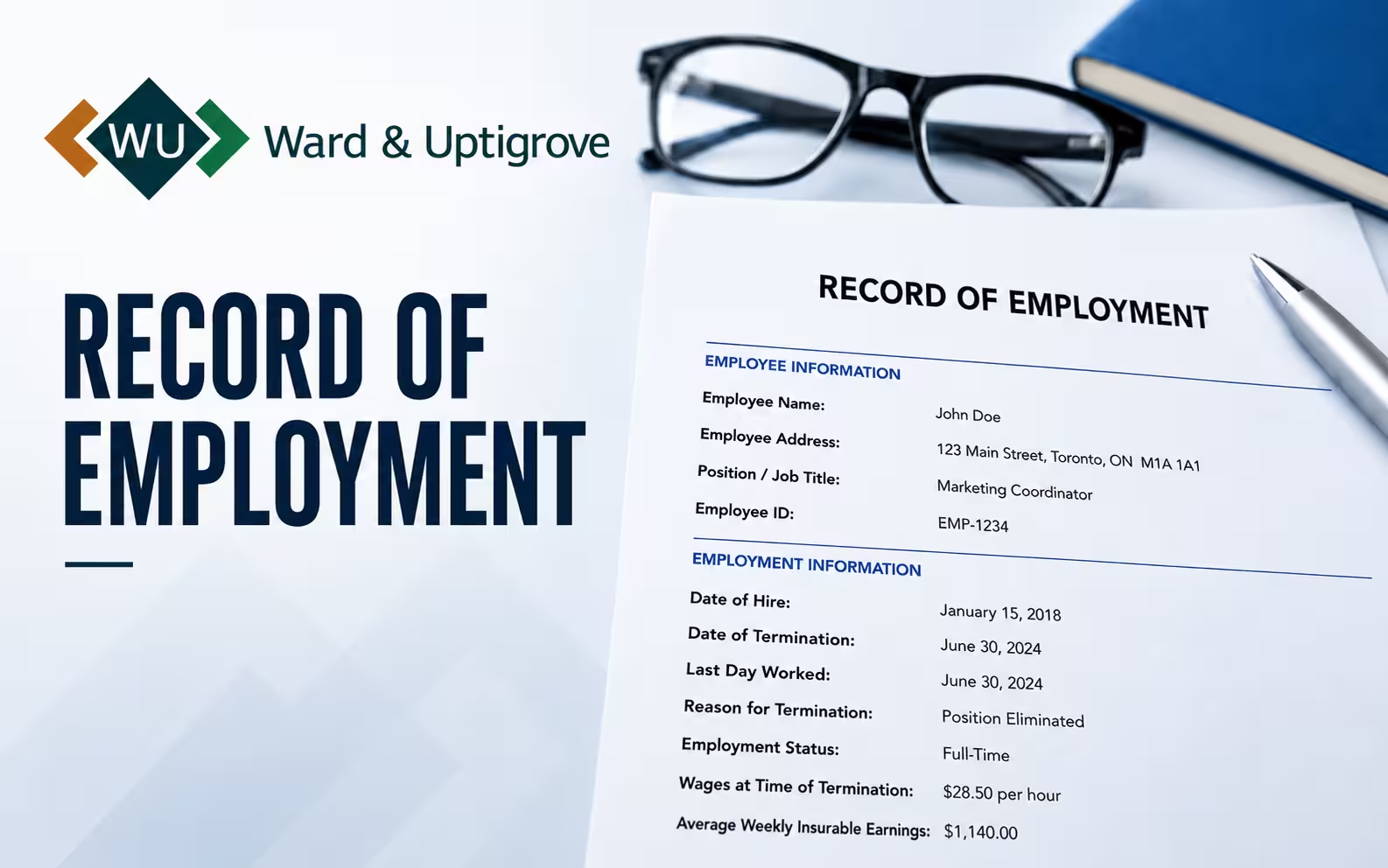

Records of Employment (ROE)

Records of Employment (ROE) – When to Issue and Why Records of Employment are a common document that are required to be filed with Service Canada by any employer in any industry that has employees. This document can be filed electronically through ROE Web with Service Canada or by requesting paper ROE from Service Canada.…

-

We’re Attending the 2026 CVMA Convention

The Ward & Uptigrove Veterinary Advisory Group will be attending the CVMA Convention at the Delta Hotels Prince Edward in Charlottetown, PEI, from June 25 – June 27. Jon Soltys and Brendan Magee will be representing Ward & Uptigrove at Booth 402. Be sure to stop by and say hello if you’re attending the convention.

-

Farm Succession: Planning Beyond Today

Farm succession planning is not just about the future – it is about protecting what you have built and ensuring a smooth transition for the next generation. Ward & Uptigrove’s Agriculture Group is hosting a complimentary presentation, Farm Succession: Planning Beyond Today, designed to provide practical guidance on navigating the financial, tax, and family considerations…

-

Ensuring the Appropriate Insurance Coverage: A Key Part of Financial Planning

When people think about financial planning, they often focus on investments, retirement savings, and tax strategies. While these are all important, one of the most critical elements of a sound financial plan is often overlooked: protecting your family’s financial security if life takes an unexpected turn. For many households, the greatest financial risk is not…

-

Southwestern Ontario’s Top Employer Award 2026

We are pleased to announce that Ward & Uptigrove has been selected as a recipient of the 2026 Southwestern Ontario’s Top Employers Award. The award is based on the following criteria: 1. Workplace, 2. Work Atmosphere and Social, 3. Health, Financial and Family Benefits, 4. Vacation and Time-Off, 5. Employee Communications, 6. Performance Management, 7.…

News & Updates

Stay informed with our latest articles and news updates, featuring in-depth analysis and expert commentary.

Search News:

Loading…