Individual Pension Plans (IPP)

July 5, 2023

Dramatically boost your retirement assets with tax-deductible corporate contributions

How an Individual Pension Plan (IPP) works

An IPP is a tax-deferred savings vehicle used to invest and save for retirement. Contributions are tax-deductible and made directly from the corporation. Similar to an RRSP, the assets inside an IPP are tax-deferred until withdrawn, at which time they are treated as income.

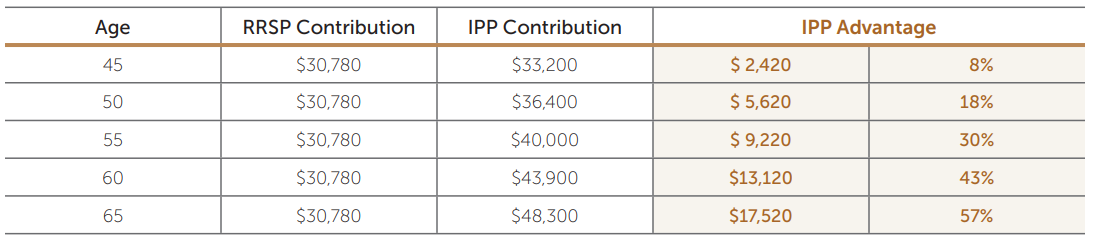

How much can be contributed to an Individual Pension Plan?

Who is a good candidate for an Individual Pension Plan?

Business Owner

Registered Professional

Middle Aged Adult

T4 Earnings of $100k+*

*an IPP can be established for someone with lower earnings

Case Study

A business owner, aged 55, incorporated for 24 years, maximum T4 earnings of $178,600 with a current RRSP balance of $291,866.

- $156,600 in immediate past service funding, tax-deductible to the company

- $221,700 in qualifying transfer (from existing RRSP balance)

- Up to $446,211 more in tax-deductible contribution room over working years (excluding past service)

- The IPP balance could be up to $1,306,700 more than the RRSP balance

All the above figures are based on 2022 prescribed assumptions.

Advantages of an Individual Pension Plan

- Increased tax-deductible contribution room – up to 65% more than an RRSP

- Can reduce passive income in corporation

- Tax-deductible company contributions for prior years (past service)

- Richest benefit plan in Canada – 2% defined benefit pension plan

- All costs are tax-deductible to the company

- Creditor protection

- Increased corporate and personal tax savings

- Can include employed family members and pass on wealth to the next generation

Next Steps

Contact a Ward & Uptigrove Wealth Management representative at 519-291-3040 or email info@w-u.on.ca to learn more.

As we near the end of Tax Season, please note our office hours below: Hours until April 29th Mon, Tues, Weds, Fri: 8:30 am - 5:30 pm Thursday: 8:30 am - 8:00 pm Saturday: 9:00 am - 12:00 pm Sunday: Closed Hours on April 30th 8:30am – 5:00pm Hours May 1st – May 2nd Closed Hours beginning May 6th Monday – Thursday: 8:30am – 5:00pm Friday: 8:30am – 4:30pm

We are th rilled to announce Ward & Uptigrove was selected as a recipient of the Southwestern Ontario's Top Employers Award for 2025. The award is based on the following criteria: 1. Workplace, 2. Work Atmosphere and Social, 3. Health, Financial and Family Benefits, 4. Vacation and Time-Off, 5. Employee Communications, 6. Performance Management, 7. Training and Skills Development, 8. and Community Involvement! Here are some of the reasons why Ward & Uptigrove was selected as one of Southwestern Ontario's Top Employers (2025): Ward & Uptigrove increased its full-time workforce in Canada by over 13 per cent in the past year and lets everyone benefit in the company's success with profit-sharing -- the company also offers generous referral bonuses of up to $5,000 per successful candidate as an incentive for employees to recruit friends Ward & Uptigrove hosts three major social events each year, giving employees the opportunity to unwind and connect with food, beverage and entertainment covered by the firm's partners -- events include a post-tax season party (employees plus a guest), a fall golf tournament, and an annual holiday celebration Ward & Uptigrove matches employee donations in kind, and encourages them to lend a helping hand in the community with a paid day off to volunteer Emily MacRobbie, human resources manager at Ward & Uptigrove, says clients appreciate the close connections and sense of care their small-town environment fosters. “We’re big enough to attract and retain some of the best and brightest minds in the industry, while simultaneously being small enough that staff and clients are known on a more personal level,” says MacRobbie. “Employees really appreciate the flexibility the firm offers, such as work location (in office or hybrid) and hours of work arrangements. We keep a pulse on what’s happening and make sure we remain competitive with things like paid time off and flexible health benefits.” To learn more about career opportunities at Ward & Uptigrove visit www.wardanduptigrove.com/careers

Accounting