John Collins, CPA, CA

Partner

Please Note Our Holiday Shutdown

The offices of Ward & Uptigrove will be closed from 3:00 pm on Friday, December 23rd and reopening in the New Year on Tuesday, January 3rd.

During the year, the Government of Canada enacted the Underused Housing Tax (UHT) Act. This Act implements an annual 1% tax on the value of vacant and underused residential properties directly or indirectly owned by non-resident, non-Canadians.

Unfortunately, the UHT Act will impact all our corporate, partnership and trust clients which own residential property. Given the broad application of the UHT Act, it is surprising it has not received the appropriate attention by Canadians.

Selected key facts:

There is much more to this legislation than the selected summary above. The purpose of this article is to inform our clients of this legislation and new filing requirement. We will send an update once the Canada Revenue Agency has released the forms for the annual return.

In January, Ward & Uptigrove will start to identify our affected clients. As we cannot guarantee we will be able to identify all our clients that will be impacted by the UHT Act, please contact your Ward & Uptigrove advisor if you:

Since 2018, the Department of Finance proposed to implement a requirement for trusts to file a T3 Trust Income Tax and Information Return and provide additional information. The proposed rules were initially expected to apply to 2021 and subsequent taxation years. Since then, these rules have been delayed twice with the new trust reporting rules now applying to trusts with taxation years ending after December 30, 2023.

Two significant parts to these new trust reporting rules are the following:

Examples of where bare trusts could exist include, but are not limited to, the following:

With the recent delay of implementing these new trust reporting rules, taxpayers have one more calendar year to prepare for the above changes.

It is important to note with the new trust reporting rules, there will be two new penalties to consider:

If you are aware of the existence of a bare trust arrangement, please let us know as soon as possible so we can properly gather all the required information in preparation for these new trust reporting rules.

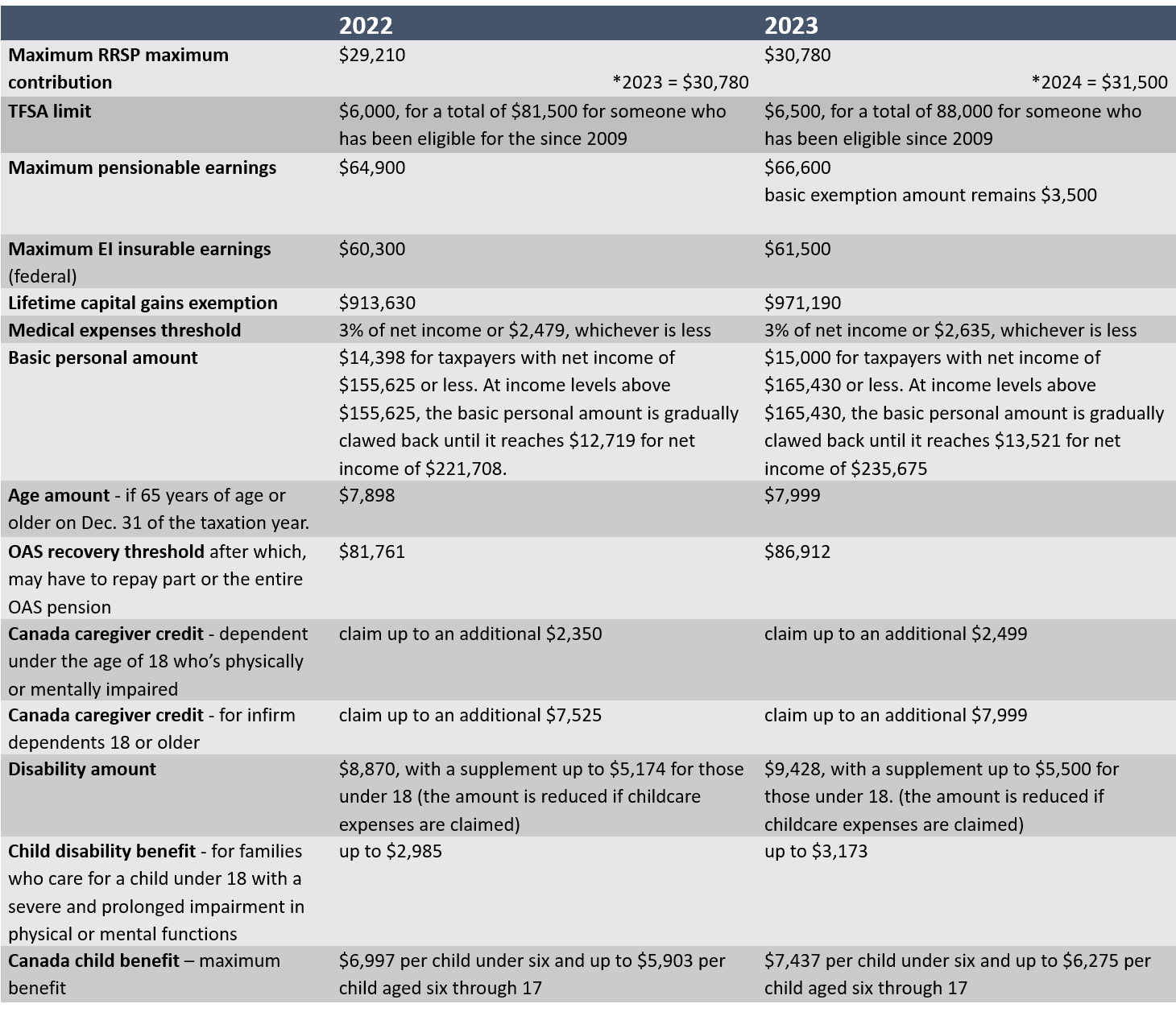

Some key amounts for 2023 that have been increased due to the 6.3% indexation increase:

*for more numbers, see the table below

Interest rates for the first calendar quarter of 2023 will be increasing to:

As of writing this article, the 2023 automobile allowance rates have not been released by the CRA yet.

As noted in our summer 2022 newsletter, the eligibility period for acquiring eligible property by a Canadian-controlled private corporate will end on December 31, 2023. Individuals and Canadian partnerships have one additional year, being December 31, 2024, to acquire eligible property.

The eligible property must be considered available for use by the above noted dates.

As noted during our summer 2022 newsletter, we require the company key for all our corporate clients in order to be able to continue to file the Ontario annual information return. While our administrative team has been following up with our clients during the past year regarding these letters, we are still waiting on responses from many of you. If you have not provided us a copy of the company key letter, please do so as soon as possible.

Included in Bill C-32, which is now considered law, is the Tax-Free First Home Savings Account (“FHSA”) that was first introduced in the 2022 federal budget.

The FHSA is a new registered plan that would give prospective first-time home buyers the ability to save up to $40,000 on a tax-free basis.

Some key elements to the FHSA:

There are many other rules to the FHSA. The above is intended to be a brief summary of this new registered plan that will be available in 2023.

Included in Bill C-32, which is now considered law, is the new anti-flipping rules for residential property that was first introduced in the 2022 federal budget. Starting January 1, 2023, profits from disposition of residential property that was owned for less than 365 days will be deemed to be business income and not capital gain that may then be eligible for the principal residence exemption.

Exceptions to this new proposed rule are the following:

It is important to note that even if one of the above exceptions apply, or if the property was held for 365 days or more, it still remains a question of fact whether a gain on a residential property sale would be taxed as business income or a capital gain.

In June 2022, the federal government enacted a change to the Income Tax Act to expand the criteria for eligibility for the Disability Tax Credit (DTC) for individuals with either:

With this change, any Canadian with type 1 diabetes will automatically be approved for the disability tax credit, under the expanded life-sustaining therapy category. This eliminates the previous requirement to prove care exceeding 14 hours per week.

The DTC is a non-refundable tax credit helping those who qualify, or their caregivers, to offset some of the costs associated with the disability. Qualification for the DTC can also open the door to additional federal and provincial programs such as the:

CRA is encouraging all who qualify to apply prior to filing their 2022 personal income tax return (T1) to avoid any delays in assessment. A medical doctor is required to complete Form T2201 for submission to CRA. If applicable, in some cases the DTC can be applied to your prior years returns, as well.

Each year, near the end of November and into December you should review if your taxable income will be higher than normal for 2022.

Please review the options below which could be used to minimize your tax liability:

It is important to note that the options above act as a tax deferral, meaning you are reducing taxes in the current year, but you should expect to pay the taxes at some point in subsequent years.

If you need assistance with tax planning this year, please reach out to your Accountant to go over the options that works best for you.

Canadian-controlled private corporations are eligible to receive a 10-20% refundable tax credit if they purchase, construct or renovate a building (included in Class 1 or 6) over $50,000 and up to $500,000. The max credit available for additions in the periods below are:

This credit is available for each fiscal year in the qualifying period.

The building investment must be made in a designated region to qualify for the tax credit. The credit is issued based on the building location not the location of the corporation’s head office. Please note that any investment in Wellington County WILL NOT qualify for this tax credit as it is not in the designated region. A full listing of the designated regions are located on Ontario’s website.

If your company is a part of an associated group of companies, only ONE company in the group can claim the tax credit each year. The other companies in the associated group will need to elect in writing to waive their right to claim the ROITC.

PEFIP is a 10 year program to support on-farm investments in:

Producers who held quota on January 1, 2021 must register with the program prior to submitting a project application. The registration process is to validate your license information and confirm your maximum funding.

Funding is determined by the amount and type of quota holdings. Young producers (35 years and younger on Jan 1, 2021) are eligible for an additional cost share.

Applicants may apply for eligible activities that started on or after March 19, 2019 and costs that were incurred on or after March 19, 2019. Applicants may submit more than one Project Application prior to the program end date of March 31, 2031 providing the applicant does not exceed their maximum funding.

For assistance with registration or submitting a project application please contact your accountant. For applications submitted to date, the timeline for receiving funding has been about six months.

The applicant guide can be viewed by following

this link.

The new section of accounting standards providing guidance on accounting for agricultural inventories is effective for fiscal periods beginning on or after January 1, 2022.

This new section will require a distinction be made between agricultural inventories and biological assets with each being reported separately on agricultural producers' financial statements. Agricultural inventories can be measured at their cost or net realizable value. Productive biological assets must now be initially measured at cost and in most cases will be recorded as long-term assets on the financial statements as opposed to being recorded as inventory and a current asset.

Productive biological assets are:

Agricultural producers’ financial statements will now include additional disclosure requirements for any biological assets and agricultural inventories. Transitional provisions will be considered for each client to reduce the administrative time in applying these new reporting standards. Your accountant will review the effect of the new standards with you during the preparation of your year-end financial statements.

As an entrepreneur, you and your team’s ability to develop and maintain relationships is a key factor for business success. In a labour market where candidates have so many employment options; effective leadership skills will help you build trusting relationships and keep your people engaged and motivated. Forbes’ article: “10 Essential Leadership Skills Every Entrepreneur Should Continually Hone” lists the following:

W&U’s

Emerging Leaders Development Program helps participants elevate their leadership skills in all the areas listed above. For more information on our Emerging Leaders’ customizable program or to register for our February 2023 upcoming online program,

click here. With W&U’s integrated services, we are here to help you achieve your business goals.

As of October 11, 2022, employers with 25 or more employees are required to have a written policy on the electronic monitoring of employees. The policy must establish whether the employer engages in electronic monitoring of employees, and if so, how. The policy must also describe in which circumstances monitoring occurs, and for what purpose the information obtained through electronic monitoring may be used.

Employers are to provide the policy to staff within 30 days of starting in their position, within 30 days of policy in place, and within 30 days of any changes to the policy.

The policy, however, does not:

Contact

HR Solutions with any questions you may have about electronic monitoring in the workplace.

Did you know minimum wage increased in Ontario as of October 1, 2022?

General minimum wage is now $15.50/our in Ontario.

Visit

Ontario.ca for details, or contact a W&U Human Resources advisor to learn more.

If you’re retired, or soon to be, you’re likely a Canadian baby-boomer. You are seeking more information about your retirement beyond merely finances, and advisors are uniquely positioned to provide you with additional retirement insight and planning.

Currently, Canadians aged 65 years old, can expect to live an additional 22 to 24 years, on average. Not only are people living longer, they are leading more active retirements. Achieving success in retirement no longer requires the bills to be paid, and to sit at home awaiting the arrival of the grim-reaper!

To gain access to the investable assets today, and manage them into retirement, advisors should examine their clients in a broader, more complete perspective.

| Retirement Element | Ready to Retire | Not Ready |

|---|---|---|

| Vision | • Unified view of retirement by both partners • Active/equal trade-offs • No surprises • Guided decision-making for all Retirement Elements | • Costly and scattered decision-making for other elements (below) • Delayed decision-making for investments and accounts • Anxiety over end-of-work |

| Health | • Health considerations not informing Interests, Social or Lifestyle elements • Critical Illness, healthcare benefits and/or savings in-place | • Successful and active retirement unattainable if health matters are not addressed, fitness promoted • Unpredictable and high healthcare costs could financially cripple retirement |

| Interests and Social | • Activities and friends independent from work, or maintained by choice • Increasing curiosity for hobbies and relationships | • Little or no plans to fill approximately 2,000 hours per year previously spent at-work • Boredom leading to increased health risks |

| Lifestyle | • Activities of daily living planned for all life-stages • Living integrated with family and friends, along with mutual activities and family events | • Days passing from one to the next without purpose, interaction or accomplishment |

| Home | • Accommodation needs understood for various phases of retirement, mobility and wellness • Costs anticipated, free capital identified • Vacation home transfer planned, with life insurance if necessary | • Home does not match Interests, Social or Lifestyle needs • Costly modifications avoided that could improve quality of life • Inexpensive modifications not planned, destroying peace of mind and quality of life |

| Legacy | • Final wishes to be followed • Tax liability at time of transfer accounted for with insurance, for example, and/or planned • Wills, Powers of Attorney considered and constructed to fulfill final wishes precisely | • Unequal or missed distribution of assets and heirlooms • Tax surprises require disposition of assets (like family cottages) to pay terminal return • Tax bill nominally higher without planned giving while alive |

Without planning that includes more elements than just finances, retirement and the years leading up to it can be anxiety laden. The period that should be relatively carefree will be the opposite.

Financial planning is a critical element of all retirement plans, but an analysis that focuses solely on money will not prepare you for a successful retirement. Additional items like those mentioned above must also be addressed.

The stress and worry of wondering if you are prepared for retirement can significantly impact your daily life.

Are you on the right track?

What are you missing?

Will you have to delay retirement?

A retirement plan, while seemingly daunting, does not have to be so intimidating, nor expensive.

Tamara Campbell, Wealth Management Advisor has been with Ward & Uptigrove Wealth Management (WUWM) for 7 years and is available to help you answer those hard questions.

At WUWM, you can now get a basic retirement plan for a discounted, flat rate of $999. You don’t have to invest, and you don't have to move accounts.

Peace of mind and savings you cannot afford to miss. Learn more here or contact WUWM.

The RRSP Contribution Deadline is March 1, 2023.

What do you need to know?

Contact your

Wealth Management representative with any questions you may have.

The Partners of Ward & Uptigrove are proud to share that Luke MacLennan was appointed the new President of Ward & Uptigrove Wealth Management earlier this year. Luke takes over the role from Mich Landry who, after serving as the President of the organization for nearly 30 years, wants to reduce his workload, while still being able to be continue to serve his clients as their Wealth Management Advisor.

Luke joined Ward & Uptigrove Wealth Management in 2016, bringing over 10 years of experience in the wealth management industry. Previously, Luke worked with the firm’s related portfolio management company, Independent Accountant’s Investment Counsel Inc. where he served on the organization’s management team.

Looking ahead, Luke is excited to have the opportunity to lead the wealth management division of Ward & Uptigrove and will ensure the primary focus of the organization will be to continue to provide clients with the highest level of service.

As 2022 comes to a close, we reflect on our 64th year of growth and progression with our staff. We are proud to congratulate the following staff members on their development and progression into new roles.

We are excited to announce that, effective January 1, 2023, the Partnership will grow by three.

John Collins, CPA, CA

Partner

Jon Soltys, CPA, CA

Partner

Pete Verbeek, CPA, CA

Partner

We would also like to congratulate the following staff members on taking the next steps along their leadership journey. We look forward to seeing these individuals continue to develop and progress within the firm, and we thank them for their ongoing contributions.

Alicia McDonald, CPA, CA

Principal

Garrett Topic, CPA, CA

Principal

Mark Woynillowicz, CPA, CA

Principal

Shayna Gibson

Accounting Supervisor

Venice Dela Sierra

Junior Accountant

Sharlene Dowdall

Accounting Manager

James Hruska

Intermediate Accountant

Ahmed Makhtoum

Intermediate Accountant

Cam Ridgway

Accounting Supervisor

Mark Tasker

Senior Accountant

Chris Hawkins

Custodian

Tina Giesbrecht

Administrative Assistant

Haley McKinley

File Clerk

Tori Jamieson

Intermediate Accountant

Cheryl Laffin

Senior Bookkeeper

Dianne Nonkes

Bookkeeping Team Lead

Sharlene Dowdall

Senior Accountant

Curtis McLaughlin

Accounting Supervisor

Jackie Landman

Administrative Assistant

Pete Verbeek

Principal

Amanda Bekkers

Intermediate Accountant

Beverley Bowman

HCSA Processor (HRS)

Hollie Card

File Clerk

Tammy Coffey

Administrative Assistant

Megan Ellis

Receptionist

Erin Kurt

Accounting Technician

Ahmed Makhtoum

Junior Accountant

Josh Martin

Junior Accountant

Myra O'Seasnain

Tax Manager

Leah Sterczer

Senior Accountant

Craig Vanderheyden

Intermediate Accountant

We are excited by our continued growth, which means we are searching for qualified accounting staff to fill new roles. W&U offers incredible opportunities for personal and professional development through a long-standing mentorship program and competitive compensation packages.

We encourage all levels of accountants to reach out or join our talent community at

wardanduptigrove.com/careers. A CPA designation is not required in order to be considered. Please email

careers@w-u.on.ca if you or someone you know is looking for a change.